ADHD and Finances: Practical Steps to Build Financial Health (Part 2)

Disclaimer: This content is educational, not financial advice. I am sharing tools, perspectives, and lessons I have learned over time while navigating finances with an ADHD brain and supporting others who do the same. This is not a substitute for personalized financial guidance from a licensed professional.

Last week in ADHD and Finances: Why Financial Wellness Feels So Hard (Part 1) I highlighted some of our ADHD traits that can make financial wellness feel difficult, as well as some ways to work with your brain.

Keep those concepts in mind as we dive into Part 2, ADHD and Finances: Practical Steps to Build Financial Health.

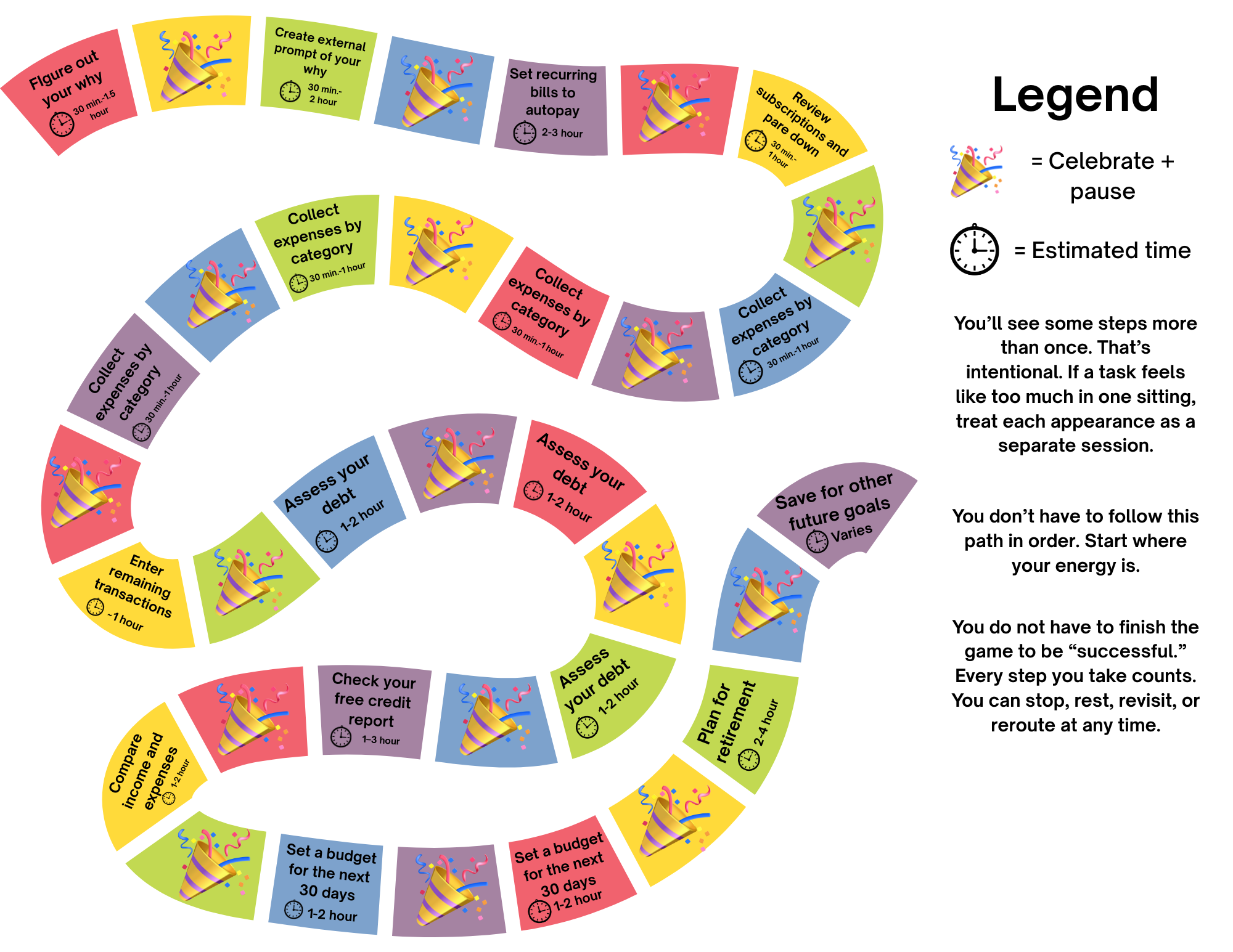

As I thought about how to present these steps in a way that actually works for ADHD brains, two things felt essential: breaking the process down as much as possible and building in intentional pauses to celebrate progress. Both help reduce overwhelm and make the process feel more emotionally doable.

I also wanted to have a version that presented the information in an easily digestible way and visually shows the individual steps. The result is the Game of Financial Health. Below are detailed explanations of each step, along with guidance on celebration. After that, you’ll find the downloadable game board.

I’ve also created a template budget that can be used in some of the steps. If you’d like to use the template budget, you’ll need to download a copy of the google sheet here. You can modify it to fit your needs.

Some thoughts as you get started

As you embark or continue on your journey toward financial health, please know that these are merely suggestions and it’s your journey. You don’t need to complete these steps in order, and you don’t have to complete all of them. Take what’s helpful, forget what’s not.

Keep in mind that many ADHDers struggle with all-or-nothing thinking and perfectionism. This is about building something workable, not optimal. Take this slow. Allow yourself to pause and reflect. You can stop after (or during) anystep.

As discussed in Part 1, finances are a heavy topic and finding motivation to tackle them can be hard. Consider enlisting an accountability partner to support you. For the steps that feel most intimidating, you might consider completing them during a body-doubling session.

Finally, don’t skip the celebration steps. For ADHD brains, progress often goes unnoticed unless there is a clear pause and some form of positive reinforcement. Our nervous systems are more responsive to immediate reward than delayed payoff, and financial wellness is almost entirely delayed payoff.

A celebration does not need to cost money, take a lot of time, or look impressive. It is simply a way to mark progress, acknowledge effort, and give your brain a small dose of dopamine so it is easier to keep going.

A celebration can be anything that feels genuinely rewarding to you. Some examples include:

Taking a break without guilt

Making a cup of coffee or tea you enjoy

Going for a short walk or stepping outside

Listening to a favorite song or playlist

Watching an episode of a comfort show

Sending a “I did the thing” text to a friend

Writing down one thing you’re proud of

Sitting with the accomplishment for a minute before moving on

Celebrations are not rewards you have to earn by finishing everything perfectly. They are acknowledgments of effort. The goal of this game is not speed or perfection. It’s to make progress feel possible, supported, and sustainable.

Step 1: Get clear on why you’re working on financial health

Suggested time: 30–90 minutes

Financial wellness is hard to sustain if it feels abstract or “should-based.” Start by getting clear on why this matters to you.

This is not about guilt or discipline. It’s about meaning.

Ask yourself:

What would money make easier in my life?

What stress would I like to reduce?

What freedom do I want more of?

There’s no right answer, and this can evolve over time.

Celebration:

✨ You connected money to meaning.

You took time to reflect on what matters to you. That’s not small. Direction comes before discipline.

Step 2: Create an external reminder of your “why”

Suggested time: 30 minutes–2 hours

We can’t rely on memory alone, especially with ADHD. Create an external prompt that keeps your “why” visible when motivation dips.

This might be:

A phone background

A written note

A voice memo

A visual collage

A screenshot saved somewhere easy to access

For example, I created my “why” in 2019 and kept it as my phone background for a long time. My why is simple: I don’t want to give all my energy to a job. I want space to cook, read, move my body, be outside, spend time with animals, learn, volunteer, and rest without cramming life into exhaustion.

Celebration:

📌 Future-you just got backup.

You built a system that works with your brain instead of relying on memory or motivation. That’s real self-support.

Step 3: Set recurring bills to autopay (can be split up)

Suggested time: 2–3 hours

Autopay reduces decision fatigue and frees up mental space.

Think:

Cell phone

Internet

Utilities

Gym memberships

Insurance

This step alone can significantly lower stress by reducing the number of things you have to remember or track.

Celebration:

🧠 Mental clutter cleared.

You reduced decision fatigue and freed up brain space. Less to remember = more energy for living your life.

Step 4: Review subscriptions and pare down

Suggested time: 30 minutes–1 hour

Go to your debit and credit card accounts and view transactions from the last 30 days. Download the transactions and highlight recurring subscriptions. Decide which ones you want to keep, cancel, or pause.

You can add the subscriptions to your own budget or use the template I’ve provided. Cancel anything you’re no longer using, enjoying, or can comfortably afford.

This is about alignment, not restriction.

Celebration:

✂️ You chose intention over autopilot.

You looked at recurring spending with honesty and care. You’re one step closer to bringing your finances in line with the life you want to live.

Step 5: Start collecting expenses by category

Suggested time: 30 minutes–1 hour per category

Begin with the categories that feel most useful or impactful.

For each debit or credit account filter by date range and view transactions from the last 30 days. Then filter by categories, or if categories feel confusing, start with merchants instead. Enter totals into your budget or the Google Sheet provided.

Start with however many categories your energy allows. If this approach feels overwhelming, you can also choose to start fresh and track expenses nightly for the next 30 days.

Helpful categories to start with:

DoorDash (Food & Drink)

Amazon (Shopping)

Eating out (Food & Drink)

Clothing (Shopping)

Celebration:

🔍 You faced the numbers.

You gathered information without judgment. Awareness is power, even when the data feels uncomfortable.

Step 6: Enter remaining transactions

Suggested time: ~1 hour

Download all transactions from the last 30 days and enter anything not already included in your budget. This gives you a complete picture of your spending without requiring perfection.

Celebration:

📊 Clarity unlocked.

You now have a fuller picture of where your money is going. That kind of transparency builds confidence over time.

Step 7: Assess your debt

Suggested time: 2–3 hours (can be split up)

Look at debts you already know exist:

Credit cards

Student loans

Medical bills

Paper or emailed bills

List balances by category.

You can do as little or as much as you want in one sitting. Clarity matters more than speed.

Celebration:

🧾 You named the hard things.

Looking at debt takes courage. You showed yourself compassion by choosing clarity over avoidance.

Step 8: Check your free credit report

Suggested time: 1–3 hours depending on complexity

Visit AnnualCreditReport.com and download reports from all three bureaus. Compare what’s listed there with what you’ve already identified. This helps ensure nothing is missing or forgotten.

This step can feel emotionally heavy. Take breaks as needed.

Celebration:

🛡️ You protected future-you.

You double-checked the full picture and made sure nothing was hiding in the background. That’s powerful.

Step 9: Compare income and expenses

Suggested time: 1–2 hours

Compare your net income (take home pay) from the last 30 days to your total expenses.

This number tells you how much margin (if any) you have for:

Debt repayment

Savings

Future goals

If this number is zero or negative, that’s information, not a failure.

For some people, this margin may first go toward building a small emergency fund before other goals. If you’re paying down debt, this is where strategies like the snowball method can come in.

Celebration:

⚖️ You found your margin.

You learned what’s actually available to you. This step creates options, even if the numbers aren’t what you hoped yet.

Step 10: Set a budget for the next 30 days

Suggested time: 2–3 hours (or two sessions)

Using what you’ve learned, set category budgets for the next month.

Over the next 30 days:

Track expenses again

Compare actual spending to your plan

Adjust as needed

Budgets are feedback tools, not moral judgments.

Celebration:

🗺️ You made a plan, not a promise.

You created a guide, not a rulebook. Budgets are tools for learning, not tests to pass.

Step 11: Plan for retirement

Suggested time: 2–4 hours

I personally follow the FIRE (Financial Independence, Retire Early) movement and invest in low-cost total market index funds. That said, I do not know your situation, and this is not financial advice.

A good starting point for many people is contributing at least enough to get any employer match, so you’re not leaving money on the table.

If this step feels overwhelming, it’s okay to pause and come back to it later.

Celebration:

🌱 You planted future seeds.

Even small steps here matter. You thought beyond today, and that’s a big deal.

Step 12: Save for other future goals

Suggested time: varies

This might include:

Trips

A home

Large planned expenses

Sinking funds

These goals can make financial planning feel more tangible and motivating.

Celebration:

💛 You gave your goals a place to land.

You made room for joy, rest, and possibility. Money became a support, not just a stressor.

Maintenance is the game loop

Financial health is not something you “finish.” These steps can be revisited whenever life changes, income shifts, or motivation dips. The goal is not to lock yourself into a system forever, but to have a process you can return to without starting from scratch.